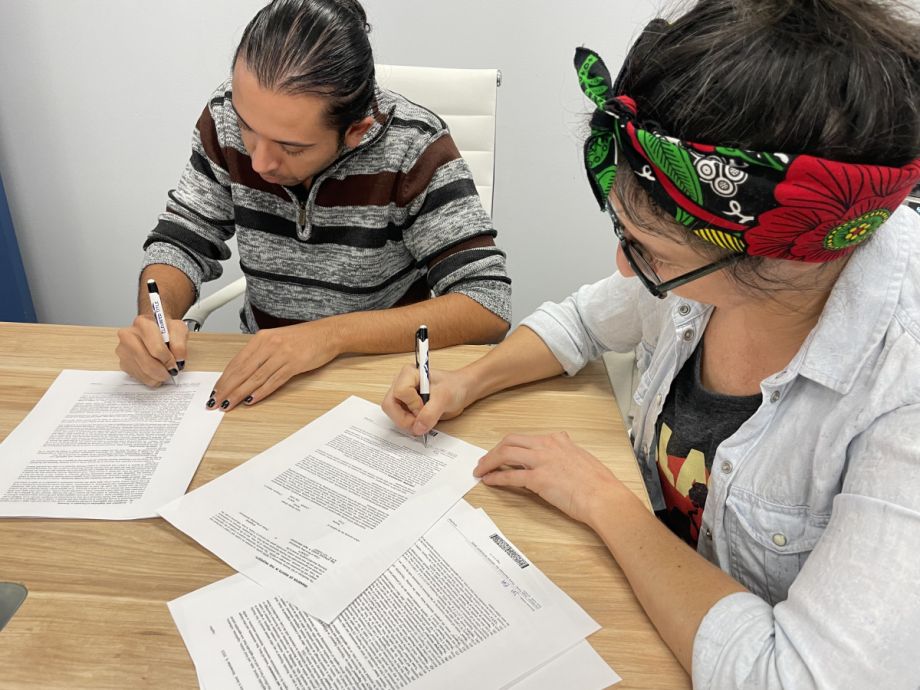

Sitting around a large conference table at an Elevated Title office in South Denver, Ellie Adelman and Jaser Alsharhan are ready to finalize their purchase of a house. It’s the first time either has bought property, and they’re visibly excited, each poised with a pen to begin signing documents.

The two have been roommates since 2018, first in a big house with six other people, and then renting a three-bedroom apartment together for the last two years. Both work in nonprofits, and they were paying $2,500 (plus $75 each for parking) a month to rent. At 2,800 square feet, with five-and-a-half bedrooms and four full bathrooms, the house they’re purchasing together has a mortgage just slightly higher than their previous rent. As long as they can rent out at least one of the rooms, if not two, their living costs will be less than renting.

Adelman and Alsharhan are part of a growing co-buying trend, where two or more unrelated, unmarried people are increasingly purchasing property together. Nationally, co-buying increased by an estimated 771% between 2014 and 2021, gauged roughly by co-owners with different last names, according to the Wall Street Journal. Companies such as Pairadime, Live Work Denver, CoBuy in Seattle, and GoCo in Toronto have emerged over the past few years to facilitate co-buying.

Working with realtor Bri Erger, one of the three agents at Live Work Denver, along with founder Laura Cowperthwaite and Sarah Wells, Adelman and Alsharhan were able to purchase a single family home at market rate in an area known for unaffordability. Denver is the ninth most expensive metro area in the nation, according to an analysis by mortgage and home equity research firm HSH. To afford a traditional mortgage, a person needs to make at least $148,000 a year, if they have 20% down. If they only have 10%, the necessary salary jumps to about $173,000.

“The single-family home dominated landscape of today’s cities represents an outdated and implicitly racist housing model that caters pretty exclusively to a nuclear heteronormative family,” says Jonathan Cappelli, executive director of Neighborhood Development Coalition (NDC), a group of affordable housing nonprofits across the Denver-Metro region. That model doesn’t correspond to the many ways people choose to live with one another, he says.

Jaser Alsharhan and Ellie Adelman with realtor Bri Erger. (Photo by Angela K. Evans)

“As a strategy, co-buying represents the decommodification of housing — radically increasing access to housing and encouraging communal forms of living. It lifts up an alternate vision of the role of homeownership rooted in collectivism and collective wealth-building.”

The co-buying model promoted by Live Work Denver and others isn’t house hacking — a way to generate passive income by renting out part of a property to cover the mortgage and make a profit. Co-buying, instead, provides an opportunity for some to escape the rental market and access the wealth generation of real estate investments. While most people who co-buy are drawn to it initially by the affordability aspect of it, Erger says, they soon realize the benefits of communal and community living.

“Traditionally speaking, people think I need my own space and my own property and my own thing. But if you’re trying to counter the capitalistic norms regarding ownership, I think this is a really good option,” Alsharhan says. “Personally, I know I live better with people around. I feel like I’m a part of something bigger than myself and also it feels good to feel supported.”

Independently, both Alsharhan and Adelman say they may have been able to buy their own condos in Denver if they had wanted. “But because we’d been around so many great examples of co-buyer power, we realized if we pooled our resources that we could afford something bigger,” Adelman says.

Co-buying power

In its quarterly Cobuy Curious Class, the team at Live Work Denver says co-buying allows people to buy “more house with less money.”

Take two different houses on the same street. One is two bedrooms and one bath, 1,050 square feet and listed for $615,000. The other is double the square footage with four bedrooms and two bathrooms, listed for $749,000. With two buyers on the larger property, both the down payment and monthly mortgage cost are roughly a third per individual compared to that same individual buying the first option. Essentially, purchasing together saves each buyer $24,000 in down payment and $1,186 monthly.

Wells’ first clients, five years ago, were three unrelated adults. One was a single artist who had enough for the down payment from an inheritance. The other two, both single mothers, had the stable income to pay the monthly mortgage. While none of them could afford a house on their own, pooling their resources allowed them to purchase a single family home in Lakewood, a Denver suburb.

Since 2019, the three agents at Live Work Denver have helped more than 100 people purchase equity in more than three dozen homes. In 2021 alone, they closed on 16 properties. Some co-buyers are a mixture of couples and friends, others are intergenerational families and there’s a particular niche for polyamorous groups.

“For a person without dependents, I should make more than enough to afford living in Denver,” says Shira Weiner, who purchased a home in Denver’s Park Hill neighborhood with Erger and her then-partner Niko Kirby in 2021. But in late 2020, after her landlords sold the building, she was at risk of losing her affordable rental. She started looking to buy as an individual, but quickly got cold feet, daunted by the process, responsibility and her options of small one-bedroom condos.

The house they purchased gave her an entry point into the housing market, an opportunity to equity, and perhaps most importantly, the chance to live in a place she’s excited about.

“It just makes so many more things feasible that wouldn’t be possible otherwise,” Weiner says.

Their investment isn’t equal, however. Weiner paid for an en suite bathroom, something that doesn’t benefit the other two co-owners. But it also increases her equity in the property if it is to sell. There’s also the benefit of shared maintenance costs should something go wrong. The plumbing went out soon after they moved in, and splitting the $9,000 repair costs was much less of a burden individually than it would have been for a single owner or couple.

All three are on the house title and loan as tenants in common: Each individual owns a percentage and responsibility in the property to varying degrees and their share can go to whomever they chose in the case of their death. (This is distinct from when partners and married couples buy under joint tenancy.)

While Mark, Kelsey and Cristina weren't afford to become homeowners as individuals, they were able to purchase a house together in Colorado, becoming Live Work Denver agent Sarah Wells' first co-buying clients. (Photo courtesy Live Work Denver)

“It’s our role and responsibility to help people understand that there is a way to home ownership in this wildly expensive market,” says Matt Hanson, a mortgage planner who works with Live Work Denver, presenting at their workshops and lending to their co-buying clients, including Weiner and friends. Currently, about a quarter of his business is lending to co-buyers.

The process from Hanson’s perspective differs slightly from working with a married couple. With co-buying, Hanson takes a separate loan application from each buyer, then assesses what they can purchase together. He combines the total income and the total debts, then considers the lowest credit score, before determining what the group can afford.

“The biggest difference is in the discussion is about exit strategies,” Hanson says. It’s a conversation he doesn’t typically have with married partners or couples. “I’m not opposed to people co-buying at all, even if one’s got money and the other one doesn’t, as long as they’ve got the exit plan in place.”

The importance of agreements

Earlier this year, the online platform Pairadime, which seeks to make the co-buying process accessible and scalable, surveyed 1,000 millennials. Only 4% say they want to wait until they are married to purchase a home and 36% say they would buy with someone if it allowed them to qualify for a bigger mortgage. When it comes to help from their parents, 51% of the respondents said they’d rather see that in the form of a co-investment in a property rather than an outright gift. But the traditional real estate process doesn’t often support unmarried co-buyers, says Pairadime co-founder, Joe Hoppis.

“And then when one of them wants out or there’s an exit, it’s catastrophic for everybody – for the agents, for the lenders, for the market,” he says. “Everybody suffers because we didn’t help them do it right from the beginning.”

Currently, Pairadime has about 100 agents working in cities across the U.S. and Canada — from Boston to Miami, Calgary, Toronto and some in Texas, California, Oregon and Washington. There have also been co-ownership purchases in less expensive markets, like Tennessee and Kansas, Hoppis says.

Since April, the company has helped facilitate about 80 transactions, matching co-buyers through its online survey, calculating what they can afford, connecting them with an agent and lender in their area, and helping them draft a 26-page legal agreement that protects each person’s investment and provides clear boundaries, including how expenses and equity are divided, as well as what happens if someone decides to move.

The last part — the agreement builder — is the only cost in the process, around $95, Hoppis says. The contract is viable in all 50 states and Canada, but the company still recommends a legal review.

“We believe that agreements and clarity around agreements is the best and most loving thing you can do to protect relationships,” Hoppis says.

Caitlin Alexander and Kayla Hoggatt met in yoga teacher training in 2017 and by July of that year they had bought a house together in Denver.

“We both knew that wasn’t something that either of us could do as individuals, but if we were to combine our finances, that it would be a possibility,” Hoggatt says.

With the help of a willing real estate agent and lender, the two were able to qualify for a Federal Housing Administration (FHA) loan in addition to a grant that helped cover the down payment. They also contracted with a lawyer to help review their co-buying agreement.

The pair sold the house in 2020 due to a variety of life circumstances, referring back to their agreement in the process to help determine how to divvy up the equity. Even though the co-buying experience was brief, both Alexander and Hoggatt are glad they did it. They were able to make about $60,000 of equity over the time they owned, and they became best friends in the process. Alexander was even Hoggatt’s maid of honor in her wedding at the end of 2020.

In the case of Weiner, Erger and Kirby, the agreements protected everyone when Erger and Kirby split up; the shared goal of community and building equity remained intact.

“[The breakup] was probably the very easiest because of the structures,” Kirby says. “Not a lot was renegotiated or unclear because we had the contingencies.”

While encouraged by the realtors at Live Work Denver, lenders like Hanson and Pairadime, there’s nothing regulatory that requires co-buyers to use an agreement. And in the end, not every client signs one.

Alsharhan and Adelman moved into their new house at the end of November and have yet to sign theirs. But they are in discussion over its contents and plan to have a legal review soon. It covers everything from splitting up their equity shares relative to the square footage they occupy in the house, to a monthly contribution in a shared bank account for emergency repairs and a commitment to co-own for at least five years.

Disrupting the game

Agreements can help mitigate a lot of the issues co-buying can present — everything from how finances are split, to responsibilities around the house to clear exit strategies. It can also help surface issues, like disconnection over preferences with noise and privacy, kids or pets.

But the team at Live Work Denver has also faced other challenges as they help clients looking to co-buy.

There is still cultural skepticism around co-buying and the idea of financially investing with friends and even family, and some shame and grief that comes with the realization individual home ownership may not be accessible to everyone.

“The reality is the system does not set people up for that,” Wells says. “And so we have to grieve this version of the American dream and figure out what is accessible and available. Cobuying is one way to do that.”

Aligning people on the same timeline, when the process can take longer than traditional real estate transactions, can also be a problem. And finding the right property suitable for co-ownership can be a challenge, as can local zoning and occupancy laws. And although the Live Work Denver team often sees perfect houses for co-buying, they frequently sell before a group is ready to make an offer.

To help mitigate these challenges, Live Work Denver is in the process of setting up a rotating loan fund, with a $400,000 investment from Colorado’s Gary Community Ventures. With a mission to help families decrease expenses and build equity, the House First program will allow Live Work Denver to acquire and renovate houses well-suited to co-ownership first, and then sell them to co-buyers at cost. Any profit will go back into the fund to purchase more property.

It will be an opportunity, Wells says, for people to negotiate co-buying loans and agreements without the added pressure of the competitive real estate market timeline. The hope is historically marginalized communities will have easier access to the wealth generation investment of real estate.

So far, Live Work Denver’s clients have been primarily white queer-identifying females, the network and social circles of the brokers. But in response to Live Work Denver’s co-buying classes, the team has been asked to present within other community groups in Denver like Globeville, Elyria-Swansia Coalition and East Colfax Community Collective, local anti-gentrification organizations seeking to prevent displacement of predominantly people of color and low-income community members. They’re also working with The Center for Community Wealth Building to offer classes in Spanish in early 2023.

Hoppis, too, hopes co-buying and Pairadime can help achieve more equity in the real estate market. But Pairadime is still too new and it’s still too early to quantify demographic data of co-buyers to really understand who is taking advantage of the model.

“If we can increase marginalized populations to believe that they can and equip them with a way to do it, we’ve done it. We did something to be a disruptor in this game,” he says.

Co-buying is by no means a panacea to the affordability crisis most cities across the country are facing. The housing market does not, in many ways, reflect the true price most people can afford, as the cost of single family homes have reached an all time high. Resistance to density, a lack of inventory and jobs that pay below-living wages all contribute to the need for policies and initiatives that drastically increase affordable housing. But co-buying does provide an opportunity for some to purchase property for the first time.

“Fundamentally, local, state, and federal governments need to coordinate policy to ensure that a sufficient number of homes are built, sold, and subsidized at affordability levels that open the American dream of homeownership to a wider array of buyers,” says Cappelli, who heads the Neighborhood Development Collaborative in Denver.

But the co-buying model presents a reasonable option for many individuals and households, he says, and ought to be fostered as an alternative. “This strategy belongs as one of a host of tactics needed to bring homeownership into reach for more people.”

Next City is one of more than 20 news organizations producing Broke in Philly, a collaborative reporting project on solutions to poverty and the city’s push towards economic mobility. Follow us at @BrokeInPhilly.

This article is part of Backyard, a newsletter exploring scalable solutions to make housing fairer, more affordable and more environmentally sustainable. Subscribe to our weekly Backyard newsletter.

Angela K. Evans is a journalist exploring the intersection of systems, people and culture through the art of long-form storytelling.